This post has been subconsciously rattling around in my head since the very early days of Horolonomics.Never leave your wingman. For some reason it coalesced into something a bit more substantive over the past few days. The TLDR on this is that the existence of Veblen effects in the luxury watch market implies there are probably multiple equilibria. The economics of markets with multiple equilibria is quite different than the textbook view of markets. In such markets, expectations and herd behavior are extremely important. These can quite significantly change the price of a product, even if all market fundamentals are stable.

Before we explore these results, let's begin with some first principles. Most markets follow the law of demand: as price goes up, the quantity demanded of a product declines. As I've discussed previously, luxury markets are different. They typically "break the law" when it comes to demand: when price increases, people may actually want the product even more. We refer to this as a Veblen effect, after Norwegian-American economist Thorstein Veblen. There are many reasons why this might happen. Veblen, himself, might have attributed it to "conspicuous consumption." A high-priced object could confer social status on an individual, and the higher the price the bigger the status "halo." There is also the possibility that a high price today could signal an even higher price tomorrow (more formally, there may be positive serial correlation in prices). In this case, as price increases, speculators may be drawn to a product in anticipation of a payout from the future increase in prices. You can also think of this as the "siren song" of potential capital gains.

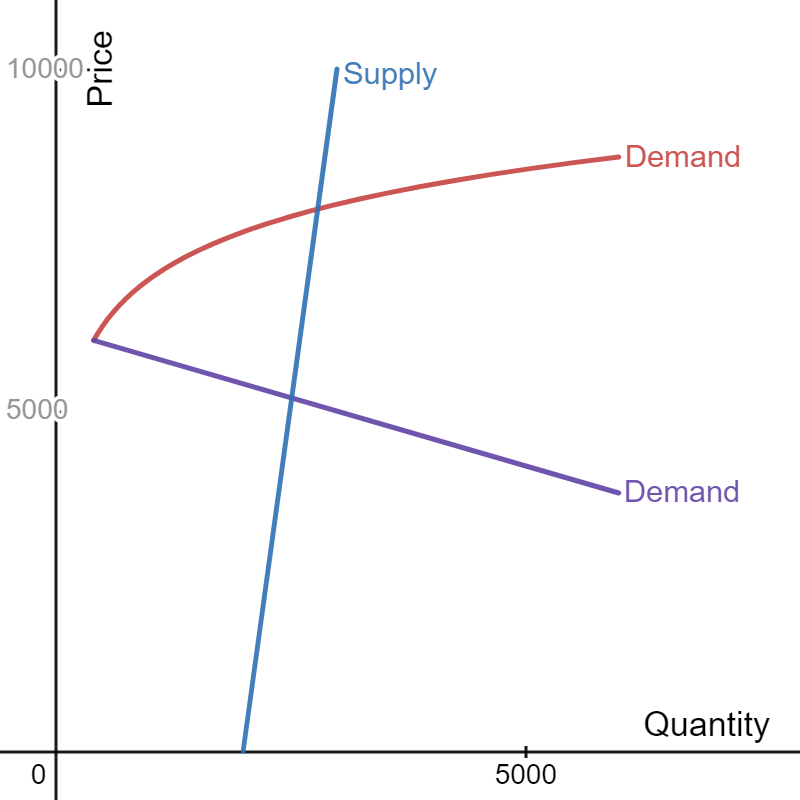

Let's turn to the market for a fictional luxury watch brand, call it Patelex.The Patelex market. Let's assume that at low prices, the law of demand holds, while at high prices Veblen effects prevail since the status / capital gain effects are larger in that region. In the figure presented here, I've drawn a demand curve that captures this notion. The purple segment of the demand curve illustrates the fact that, if prices are in the $4-$6,000 range, as price goes up, fewer are interested in buying Patelex. However, at a price of $6,000, demand begins to follow a new pattern because Veblen effects have become strong enough. Above $6,000, as price increases, still more people try to buy Patelex. Along this red segment, the law of demand no longer holds and Patelex sells more watches as the price increases.

I've also included a positively sloped supply curve (blue) on the graph, reflecting the fact that the law of supply holds. As price increases, Patelex tries to bring more watches to market. This supply curve is fairly steep, though, suggesting that supply is somewhat inelastic (it doesn't respond strongly to price).

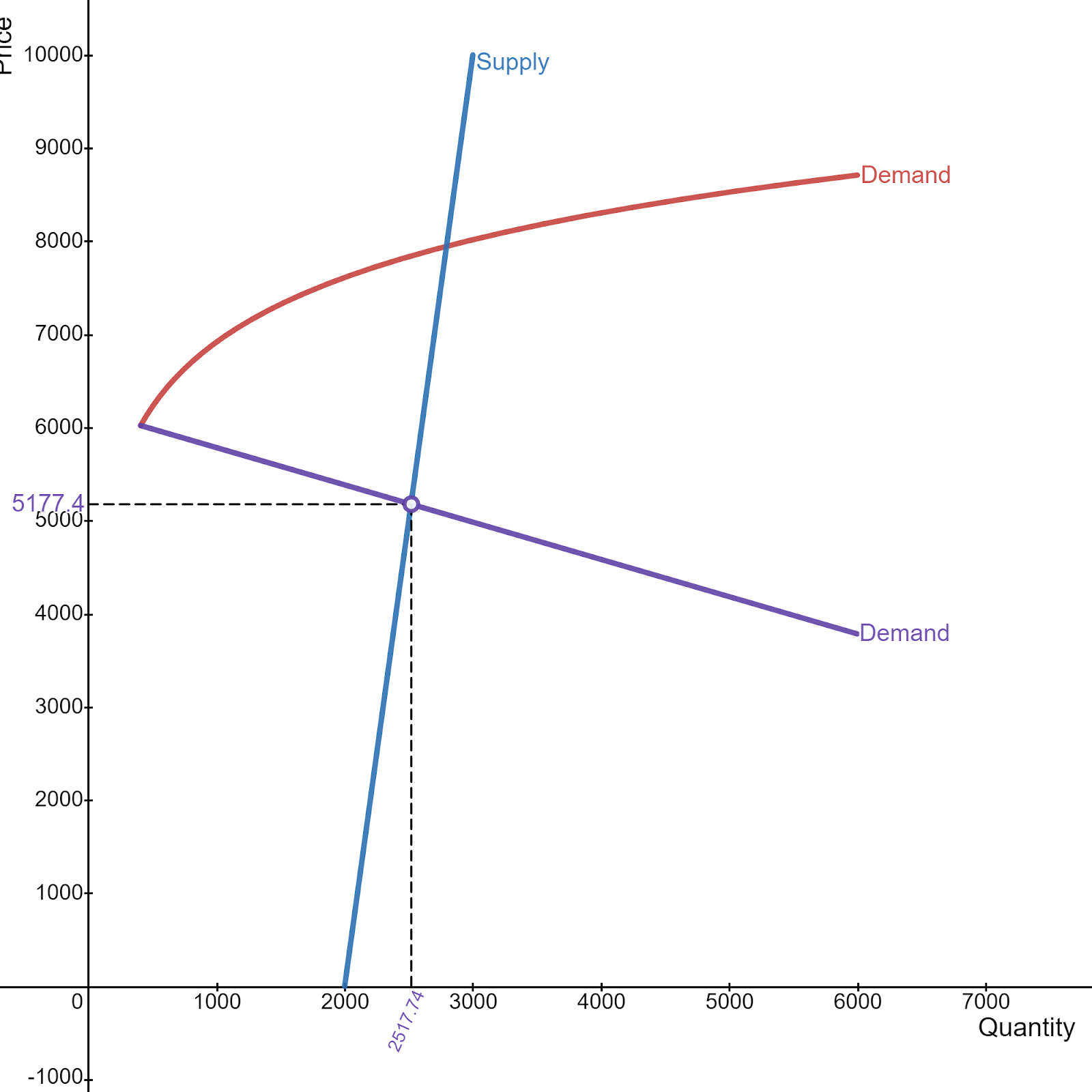

In a typical market, we tend to focus on the intersection of the blue supply curve with the purple demand curve, as indicated in the figure here. A clasic market-clearing equilibrium in the Patelex market. This is a market-clearing equilibrium, in the sense that the number of Patelex watches brought to market is equal to the number of watches demanded by buyers. In this case, the market clears at approximately 2,500 watches sold and a price of approximately $5,200.

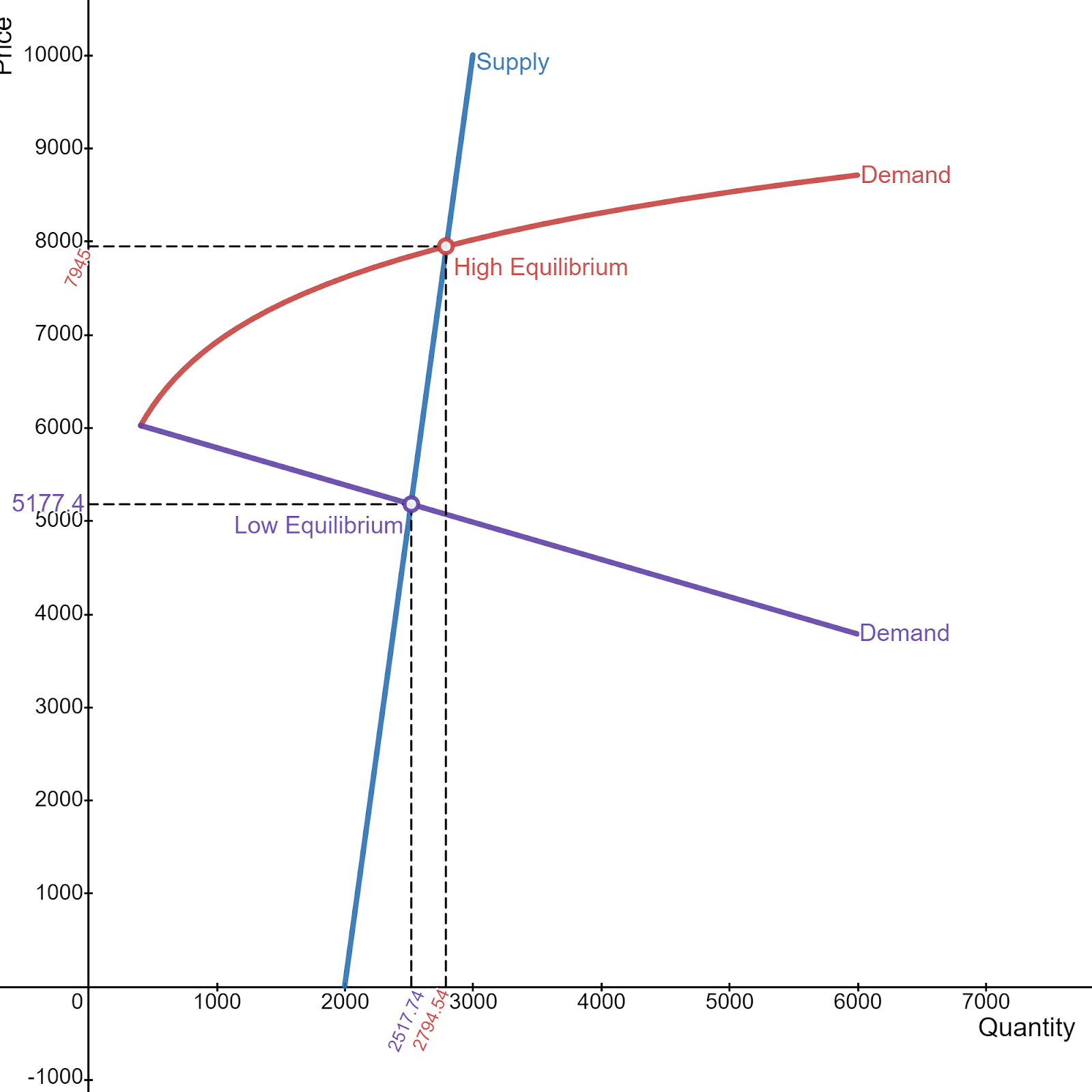

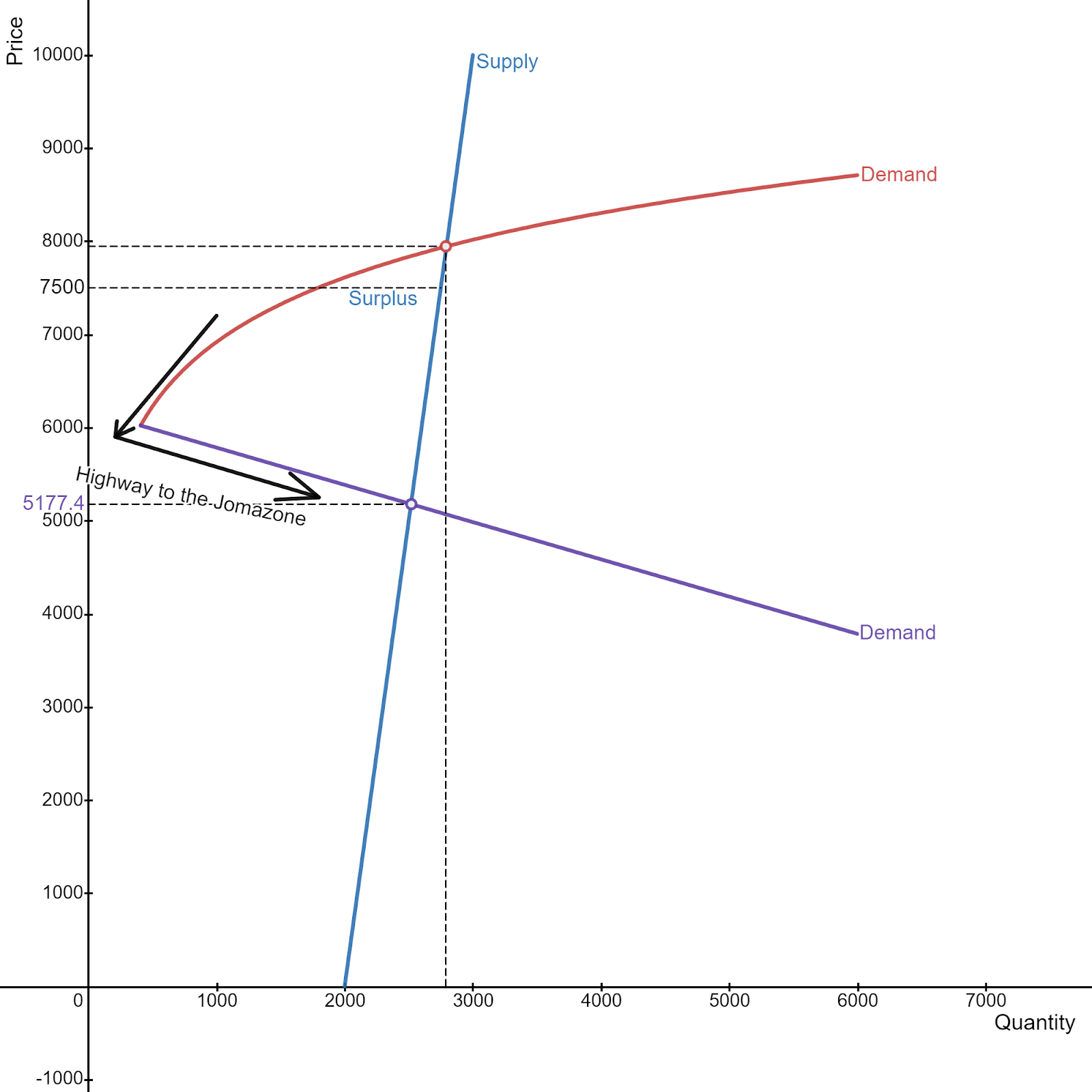

A market with Veblen effects presents a whole new collection of challenges, though. When the law of demand is irrelevant, a lot of the things we know about markets do not hold. The Patelex market with both equilibria marked. In particular, a Veblen market of the type I've described has multiple equilibria. On the graph, the second equilibrium is at a higher price where the blue supply curve intersects the red demand curve. In this case, the market clears at approximately 2,800 watches sold. However, it is actually a higher price which brings forth this additional demand due to Veblen effects. The market clears at a price of approximately $8,000, about 54% higher than the low price equilibrium

Any brand would obviously prefer the high price equilibrium. There, Patelex earns $22.4 million in revenue. At the low price equilibrium, the brand only earns $13 million, a loss of more than $9 million compared to the high equilibrium. Since the same product, with the same manufacturing costs, is sold at both equilibria, the revenue loss is a dollar-for-dollar loss of profit.

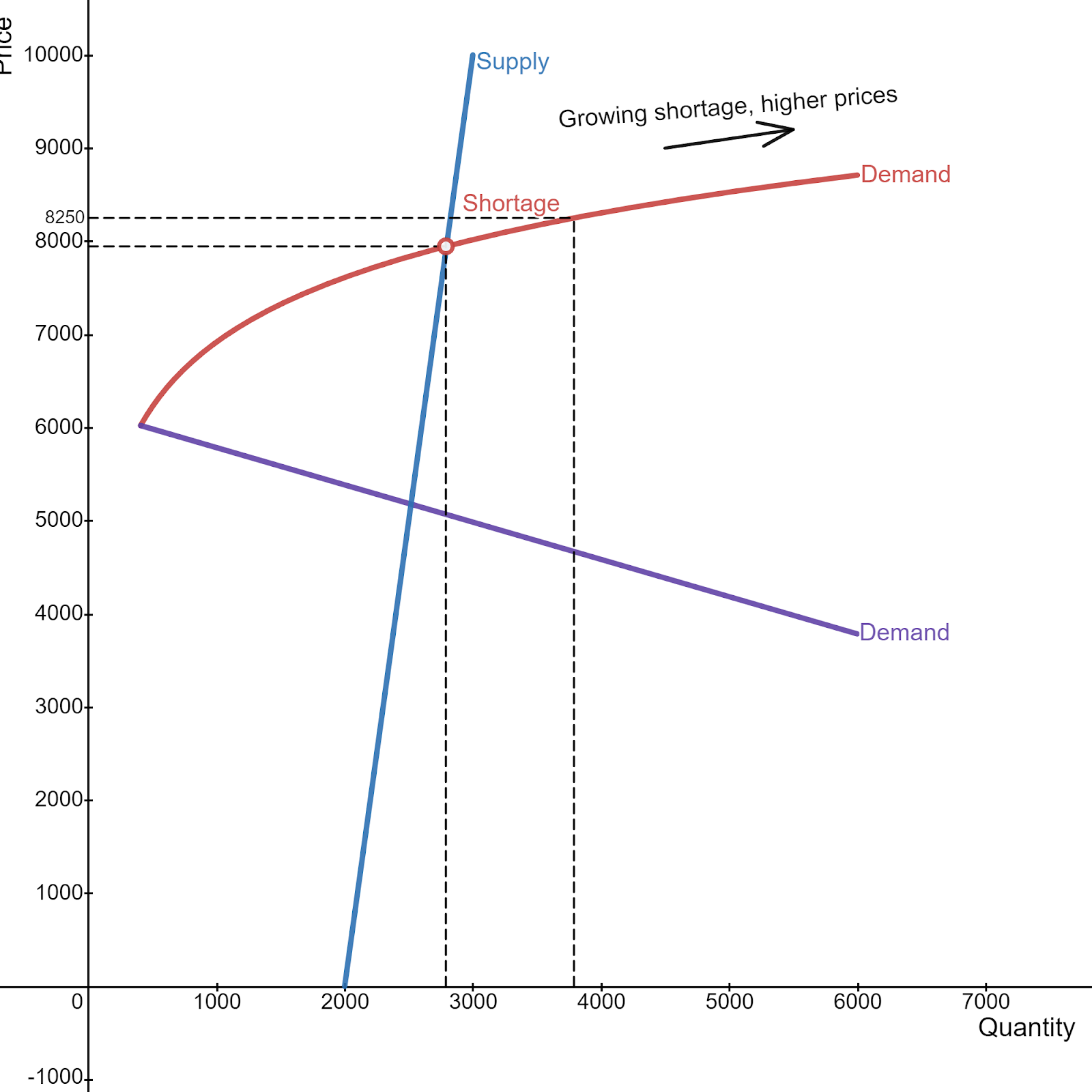

Is one equilibrium more likely to emerge than another? The answer is yes. A bubble emerging in the Patelex market. In fact, the high price equilbrium is very difficult to sustain (more formally, it is unstable). Consider a situation in which a few buyers are willing to pay just a little extra, perhaps due to the fact that they can't get a Patelex locally so they buy from a preowned source and pay a corresponding markup. If they pay $8,250, for example, there is an immediate shortage. Additional buyers, seeing a higher price, flock towards the product as a consequence of the Veblen effect and there is additional demand for approximately 985 watches. Patelex does try to produce more watches, but it only manages to produce 25 additional pieces. The ongoing shortage of 960 watches means the price increases again, and the cycle knows no end. Prices skyrocket and there are unrelenting shortages. In many ways, this is exactly what has happened with certain in-demand watch references, such as the Rolex Submariner, the Audemars Piguet Royal Oak and the Patek Philippe 5711.

The brands would almost certainly prefer this outcome to the alternative, in which the price, for some reason, starts just below the high price equilibrium, as in the figure. Patelex price decreasing towards the low equilibrium. Let's call this "Highway to the Jomazone." For example, suppose a few dealers offer Patelex at a discount of $7,500. In this case, the quantity of watches demanded falls to roughly 1,790 due to a reverse Veblen effect. There is a surplus of watches. The price falls again, the quantity demanded falls and we repeat the cycle. For the brand, some of the pain is relieved when the Veblen effect disappears completely and we reach the purple portion of the demand curve. Although price continues to fall, quantities also begin to increase.

Ultimately, the market settles at the low equilbrium discussed earlier (a price of $5,200 and quantity sold of 2,500). This equilibrium is stable. If prices go up by a small amount, creating a surplus, they return to $5,200. If they are a bit too low the shortage causes them to rise.

What we've seen is that, in a market where Veblen effects kick in at high prices, maintaining a high-price equilibrium is a fraught enterprise. Anything which perturbs prices above the high-price equilibrium value will lead to something which looks like a price bubble accompanied by unrelenting shortages. There is almost no way out of that cycle, short of convincing buyers to pay a lower price. In contrast, if prices slip below the high price equilibrium value, watches are offered at ever increasing discounts until the low price equilibrium is achieved.

The model also suggests that it is very difficult to escape the low price equilibrium. It has a gravity, of sorts, which a brand must fight to escape. Every brand would prefer to achieve the high price equilibrium and they would undoubtedly use every tool available, such as marketing and ambassadors, to convince consumers to pay that higher price. However, if they fall short, even by a little, they will return to the low price equilibrium. They also risk a "winner's curse" in which consumers pay too much and the brand is overtaken by shortages and ever increasing prices on the secondary market.

In summary, shepherding a watch brand when there are Veblen effects is extremely challenging. Even if you manage to convince buyers to pay a high price for your product, any change in pricing, high or low, can have dramatic consequences. This might explain why many of the most successful brands do everything they can to tighly control pricing while cautiously communicating with buyers and changing their products incrementally (there are, of course, exceptions). The challenge becomes even greater if your brand gains a reputation for being worth less than what you would prefer to charge. In that case, it can require a major effort to achieve the alternative, high-price, equilibrium. There are some who have made this transition, but it remains to be seen if their success is due more to their own efforts or overall market conditions.

Thanks for publishing such great information. You are doing such a great job. This information is very helpful for everyone. Keep sharing about Catalog of the Patek Philippe Museum. Thanks.

You have provided valuable data for us. It is great and informative for everyone. Keep posting always about watch straps nz. I am very thankful to you.

Last week, Icebox / Swiss Watches GA, a third party retailer of pre-owned watches, officially acknowledged receipt of a lawsuit filed by Rolex USA in the US District Court for the Northern District of Georgia - Atlanta Division. A screenshot of the Icebox / Swiss Watches GA retail location Source: Rolex's legal filing. The cause of action for Rolex's lawsuit against Icebox / Swiss Watches GA is "Trademark Counterfeiting, Trademark Infringement, False Advertising, Designation of Origin, Descriptions, Representations, and Unfair Competition." I've previously covered lawsuits of this sort filed by Rolex against independent retailers who sell modified watches. But this one is an order of magnitude different. Icebox / Swiss Watches GA has some very high-profile clientele. For example, a YouTube video from five years ago entitled "Post Malone Buys Rolex For 21 Savage & Autographs A Bugatti!" has over seven million views (the video content is pretty ...

This may not come as a surprise, but I do not read German-language newspapers on a regular basis. Dial of a vintage Omega Constellation, pie pan. I am, however, keenly interested in a scandal involving the Swatch Group and a "Frankenwatch" Speedmaster which was sold at auction a while back for over $3 million. I won't go into all the minute details here, but the punchline is that Swatch Group bought the watch only to discover that some of its own employees may have been part of a conspiracy to assemble a watch which would be quite rare and important if it were authentic. But, apparently, it was not authentic. When the deception was uncovered, various people who were part of the "inside job" lost employment and, reportedly, legal authorities were notified in Switzerland. I originally wrote about this in 2023, you can read my coverage here . There's been excellent reporting on this matter from many sources (see, for example, this story from Bloomberg). ...

Today, I received a dispatch direct from Le Brassus, aka global headquarters for Audemars Piguet. The email cautions collectors that fraudsters are targeting clients of AP and other brands with potentially bad consequences. In the interest of collector protection, and as a bit of "public service," I'm copying the main body of the AP email below. Be careful out there, always check email headers and double-check with your known contacts at any brands before wiring money, for example: "Cybercriminals are trying to scam customers in every industry and watchmaking makes no exception. At Audemars Piguet we want to be sure that our trusted community is well protected against cyber- criminal exploits. Recently, threat actors have been using spoofing techniques to send fraudulent emails pretending to come from trusted brands, such as ours, in an attempt to deceive individuals into disclosing sensitive information, making payment to illegitimate accounts or engaging in fra...

Thanks for publishing such great information. You are doing such a great job. This information is very helpful for everyone. Keep sharing about Catalog of the Patek Philippe Museum. Thanks.

ReplyDeleteYou have provided valuable data for us. It is great and informative for everyone. Keep posting always about watch straps nz. I am very thankful to you.

ReplyDelete