This post started as an investigation into whether the crypto "winter" does actually explain recent changes in luxury watch prices. I was motivated by a Bloomberg article containing this claim (as well as subsequent discussions of that article). As I started working on this post, though, I realized that the data referenced in the Bloomberg article is so bad, my plans had to change. Fam: we have a problem. People publishing numbers relating to the watch industry do not seem to understand some very fundamental concepts when it comes to markets (I'm going with this possibility rather than a rather more troubling conclusion: they understand and they're actively misleading people). Those same people are making statements and drawing conclusions based upon some very shaky foundations.

So, this post is going to explore why a lot of the numbers we see when it comes to the watch market do not actually measure prices. Many claim to report prices, but that is not what they're doing. This is becoming a bit of a theme on Horolonomics: the fact that someone has a number does not mean that number measures something you are interested in. I have a whole lot of sympathy towards those who are pushing us towards the use of data in order to understand the watch market. But poorly measured data is really no different than visiting the oracle at Delphi and having her roll the chicken bones or read the tea leaves or whatever it is she did. In fact, mismeasured data may be way worse than no data at all because it could lead you to inappropriately suspend your skepticism.

A price taking market. Not how much of watch trade works.Let's get into it. There are a lot of ways a market can be structured. One is what we might think of as "price taking." This is like the supermarket: they post a price for an item on their shelf. Then, you go in and buy it at that price. So, there is no difference between what the supermarket asks for an item and what you pay.

The important thing to note is that very few online platforms for luxury watches operate in this way. Instead, we see a whole lot of asking prices for watches. What we don't observe is the closing price: that is, the price actually paid for a watch (for that matter, nor do we observe the "bid," which is the price buyers are willing to pay). When people say "price" for an item in this type of market, what they're really thinking about is the closing price. This is the amount of money that changes hands. The closing price is an agreement between buyer and seller about the object's value.

Let me give an example of why this is a problem for so-called watch market data providers. Subdial defines their "market index" for watches as follows: "Our data model is proprietary, it is updated daily with listings from around the world." So, they basically scrape a whole bunch of numbers off of a whole bunch of watch platforms. Here's the thing: these are asks. They are what the seller wants you to pay. They are not closing prices. Closing prices are much, much harder to obtain.

Here's why this is a problem: suppose I post a vintage Omega pie pan Constellation on a watch forum scraped by Subdial. I list it for $3,000 but I know it doesn't warrant that amount. But I think, "hey, someone out there might actually go for it." Into Subdial's database goes an entry that says a Constellation price is $3,000.

Now, let's say I get a DM from someone and they say, "look, that thing is not worth $3k but I'll give you $1k for it." I give up the ruse, agree to sell at a closing price of $1k and we carry out the transaction on Venmo or whatever. I mark the listing sold in the forum. So, Subdial has the wrong number in their database. The price is the actual closing price of $1k but they record it as $3k.

No amount of handwaving is OK in this situation. The price simply is not $3k. Please know that I'm only mentioning Subdial here as an example. There are many many people now publishing mismeasured "price" data. These publications are kind of like the National Enquirer (tabloid) of economics: they get a whole lot of attention but John Travolta did not actually marry an alien (the price of a Constellation is not actually $3k).

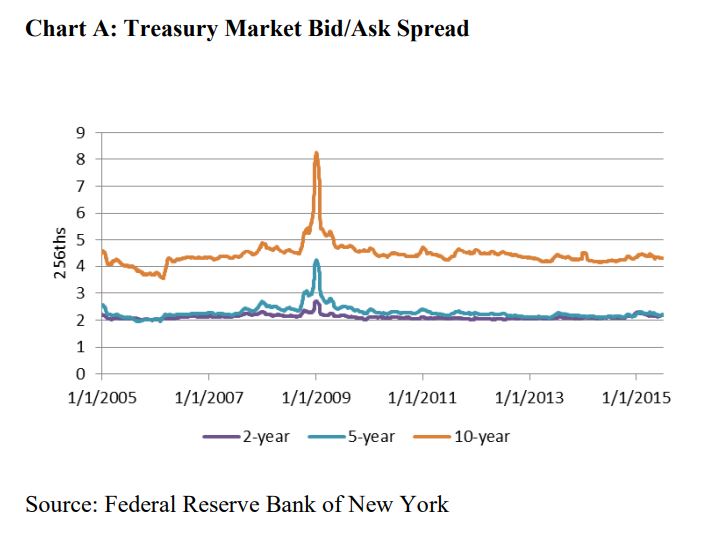

Bid ask spreads before and after the Great Recession.I know some of what I bring up here might risk seeming pedantic. But particularly now, when liquidity is lower and there is a whole lot of uncertainty due to the high risk of recession, asks are probably really really far off from closing. We know this from the US Treasury bond market, where bid ask spreads (the difference between what a seller will accept and a buyer will pay) spiked during the Great Recession of c. 2008 - 9 (see the included graph). So it's quite likely that the asks masquerading as watch prices right now are more inaccurate than ever.

I do believe that, in general, more information is better. However, it is very important that anyone publishing or discussing numbers honestly reports the limitations of those numbers. Right now, that seems far from the case when it comes to secondary market watch prices.

My book on the history of Rolex marketing is now available on Amazon! It debuted as the #1 New Release in its category. You can find it here.

This may not come as a surprise, but I do not read German-language newspapers on a regular basis. Dial of a vintage Omega Constellation, pie pan. I am, however, keenly interested in a scandal involving the Swatch Group and a "Frankenwatch" Speedmaster which was sold at auction a while back for over $3 million. I won't go into all the minute details here, but the punchline is that Swatch Group bought the watch only to discover that some of its own employees may have been part of a conspiracy to assemble a watch which would be quite rare and important if it were authentic. But, apparently, it was not authentic. When the deception was uncovered, various people who were part of the "inside job" lost employment and, reportedly, legal authorities were notified in Switzerland. I originally wrote about this in 2023, you can read my coverage here . There's been excellent reporting on this matter from many sources (see, for example, this story from Bloomberg). ...

Today, I received a dispatch direct from Le Brassus, aka global headquarters for Audemars Piguet. The email cautions collectors that fraudsters are targeting clients of AP and other brands with potentially bad consequences. In the interest of collector protection, and as a bit of "public service," I'm copying the main body of the AP email below. Be careful out there, always check email headers and double-check with your known contacts at any brands before wiring money, for example: "Cybercriminals are trying to scam customers in every industry and watchmaking makes no exception. At Audemars Piguet we want to be sure that our trusted community is well protected against cyber- criminal exploits. Recently, threat actors have been using spoofing techniques to send fraudulent emails pretending to come from trusted brands, such as ours, in an attempt to deceive individuals into disclosing sensitive information, making payment to illegitimate accounts or engaging in fra...

Last week, Icebox / Swiss Watches GA, a third party retailer of pre-owned watches, officially acknowledged receipt of a lawsuit filed by Rolex USA in the US District Court for the Northern District of Georgia - Atlanta Division. A screenshot of the Icebox / Swiss Watches GA retail location Source: Rolex's legal filing. The cause of action for Rolex's lawsuit against Icebox / Swiss Watches GA is "Trademark Counterfeiting, Trademark Infringement, False Advertising, Designation of Origin, Descriptions, Representations, and Unfair Competition." I've previously covered lawsuits of this sort filed by Rolex against independent retailers who sell modified watches. But this one is an order of magnitude different. Icebox / Swiss Watches GA has some very high-profile clientele. For example, a YouTube video from five years ago entitled "Post Malone Buys Rolex For 21 Savage & Autographs A Bugatti!" has over seven million views (the video content is pretty ...

hi

ReplyDelete