I've read a variety of reports and commentators suggesting that, unlike the majority of businesses, the watch industry may be immune to economic downturns. The analysis of economic cycles is a specialized field and it is very tricky to assess how particular industries are impacted by fluctuations. Most of the claims I've heard about the business cycle and the watch industry could benefit from more careful inspection, so I'll try to do that here.

I decided to use methodology that represents a solid "starting point" when it comes to business cycle analysis. The impact of a recession on any industry is not easily or casually measured, for reasons I will describe below. The TLDR on this is that the modern watch industry is not immune from the business cycle when we use generally accepted notions of what a business cycle represents. However, there are things that do reduce the impact of economic fluctuations on the industry: watch brands have partial immunity. I will discuss this idea first.

Shock Absorbers

In 1992, the rap group Geto Boys dropped the track "Damn It Feels Good to be a Gangster." The reality is that it also feels pretty good to be in the watch industry when times get tough. There are a few reasons why this is the case, particularly in the modern era. These days, precision mechanical watches are largely purchased by those with fairly deep pockets. Most evidence suggests that income volatility is lower at the higher end of the income distribution. There are many reasons for this, but a lot of it has to do with access to financial institutions, insurance, and the like. Since the industry's buyers have more stable income, it stands to reason that demand is correspondingly more stable. This is the first reason why downturns, potentially, aren't as impactful for the watch industry.

The watch industry is also somewhat insulated from recessions due to the unique nature of the industry itself. The supply side is more or less concentrated in one country: Switzerland. This is almost the perfect stock photo for this post. Demand for watches is globally spread across a heterogeneous array of countries and regions (albiet some locations generate greater demand than others). One of the principles of portfolio theory is that holding a diverse array of assets reduces risk. The same principle can apply to macroeconomic risks. If you sell to all, or almost all, of the countries in the world, you've built a hedge against any country-specific downturn. For example, suppose the Russian market closes (you know, theoretically). Just sell 10 more watches in 10 other countries and you'll be OK.

Dampened, Not Eliminated

At the end of the day, the industry's insulation from the business cycle is an empirical question. Unfortunately, the industry itself is not always forthcoming with useful data. I and others have relied upon numbers from the Federation of the Swiss Watch Industry FH in order to draw inferences about market conditions. Of late, FH has changed its reporting format and I know of at least one commentator who has abandoned FH data as a result. In addition, as a trade organization with direct connections to watch businesses, FH isn't necessarily disinterested in how the watch industry is publicly portrayed. I'm not aware of any specific concern when it comes to information published by FH, but the organization's mission statement does not include transparency, for example.

There is one area, in particular, in which transparency would be helpful. We know that watch brands have bought back unsold inventory and destoyed it in the past. A recent TikTok video with 1.3 million likes showing unsold handbags which Coach purportedly slashed and discarded. Data on this practice is not readily available in FH's typical reports. Destroying previously produced watches is not a "good look" from a sustainability perspective (to be fair, the Swiss watch industry is not the only business likely engaged in this practice). For example, a whole lot of energy was initially consumed in the production of these watches (with associated emmissions presumably) and still more energy is used in their destruction. Fortunately, under certain international agreements, the Swiss government is obliged to report "reimportation" of Swiss products.

A product is reimported if it is brought back to the country of origin after being exported (a bit like a round trip). Official government statistics on reimportation will capture any Swiss watch brand which buys back unsold inventory. It is really the exports net of reimportation which reflect the state of the watch industry. For example, exporting $10B of watches only to have them sit in stores and then reimporting the same watches worth $10B would suggest the industry was clearly struggling. FH statistics would show exports of $10B in these circumstances, suggesting the industry was doing well. In contrast, exports net of reimportation would show zero exports. For this reason, I will use net exports below.

An additional complication with assessing the impact of a recession on the watch industry stems from the nature of recessions themselves. In the past 22 years, there have only been three recessions in the United States. Fortunately, broad economic downturns are fairly infrequent. This complicates empirical analysis because there are few "treatment experiments," ie downturns, that we can contrast with "control" years in which an economy is normally expanding. Further, when we ask "is the recession harming the watch industry," the best response is "whose recession?" As mentioned earlier, economies are not a perfectly synchronized ballet in which everyone moves in the same direction at once. Rather, they can resemble a chaotic jumble of different trajectories. For example, in the 32 years between 1990 and 2021, there were only four in which the United States, China, Japan and the world as a whole were all underperforming at the same time. Otherwise, there was a glimmer of strong performance in some portion of the global economy.

There is one additional challenge with interpreting the impact of the business cycle on the watch industry: seasonality. Not all months are created equal when it comes to watch purchasing. For example, the end-of-year holiday season is a major source of demand for watches as gifts. When such regular patterns are present in data, there is a real risk that interpreting the numbers may create spurious results since the onset of an expansion or contraction may be arbitrarily coincident with a seasonal pattern. In the subsequent discussion I will control for this possibility.

The Evidence

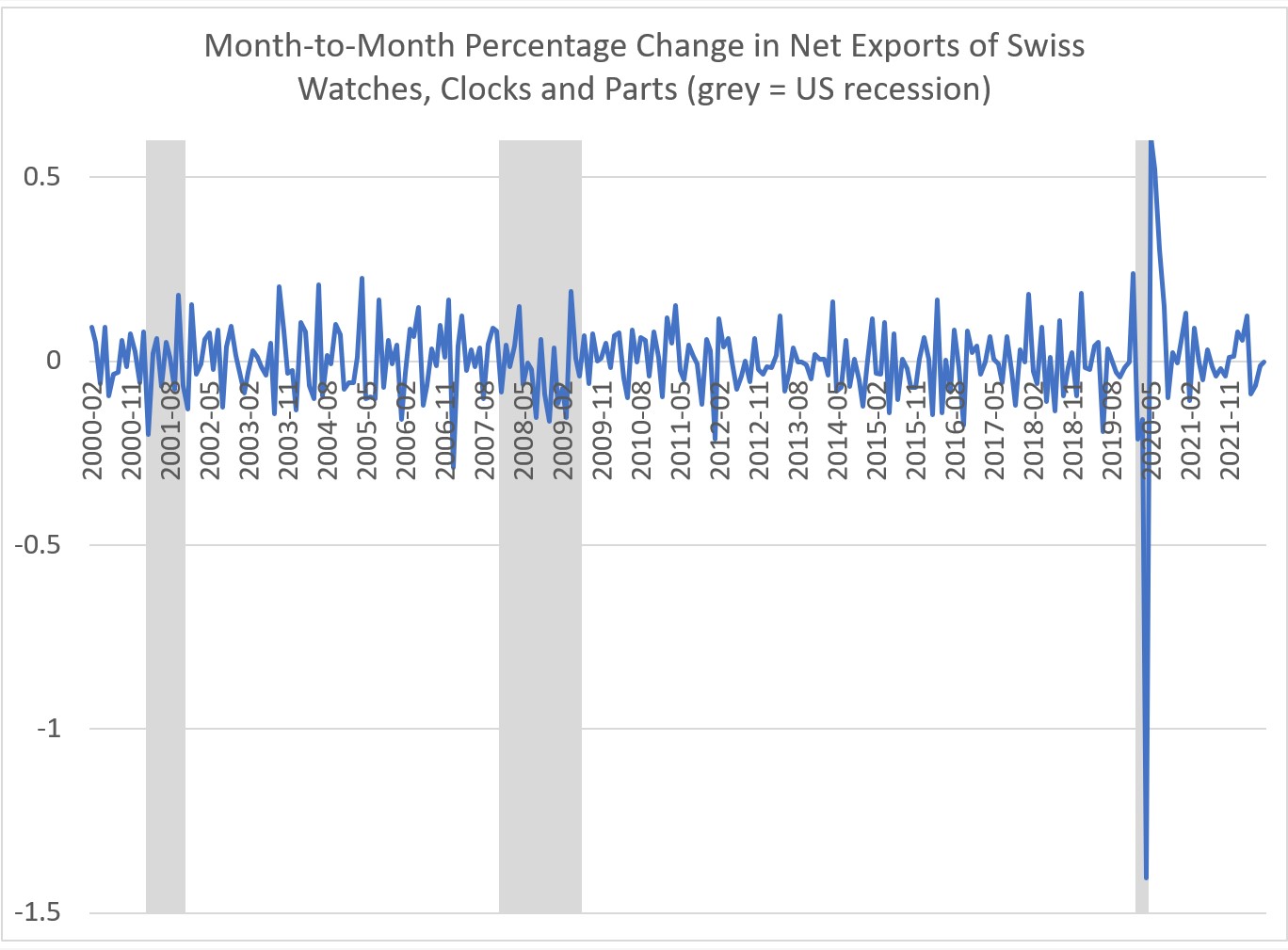

In order to assess the impact of the business cycle on the watch industry, I began by obtaining official Swiss government statistics on exports and reimportation of watches, clocks, and parts. Those numbers are available since the beginning of 2000. I then calculated net exports (exports minus reimportation) from this information. There is significant monthly seasonality in this data. For example, August net exports are quite low compared to the rest of the year. This period corresponds to the mid-to-late summer "watchmaker's holiday" in Switzerland. In contrast, the largest surge in net exports takes place in September and October as retailers stock their inventories ahead of the year-end holiday season.

I remove this seasonality from the raw data so that it will not impact my results.Net export growth of Swiss watches. The de-seasonalized net export figures are presented here. I focus on month-to-month growth in net exports (doing so removes the influence of slow-moving trends in the industry, such as dwindling sales of low-priced timepieces). The grey bars in this figure represent the official months during which the United States was in a recession (in other words, NBER business cycle dates). As I mentioned earlier, not every economy around the world experiences a recession at the same time as the United States. However, this post is a rough attempt at quantifying the cyclical nature of watch exports. In the future, I may attempt to more carefully capture the timing of global recessions.

Even visually, it is clear that the "COVID recession" had an adverse impact on the luxury watch industry. Net exports of Swiss watches collapsed and displayed their worst performance over the 20 years for which I have data. More careful inspection will also confirm that during the Great Recession of 2008-9 and the "Sept 11" recession, Swiss watch exports also languished. When I apply a formal statistical technique (an ordinary least squares regression with a dummy variable for recession months), the estimates imply that during a recession, Swis watch net exports decrease by approximately 8.4% per month. The result is statistically significant. This is a fairly drastic rate of decline. There is little doubt that the estimate is heavily influenced by the depth of the COVID recession. Nevertheless, the available evidence shows that recessions do, indeed, negatively impact the Swiss watch industry.

What Goes Up Must Come Down

There are many dimensions of the watch industry that defy norms or received wisdom. The evidence I report above, though, shows that the watch industry is like almost every other industry that is out there: when there is a recession, jobs are lost and production declines. It is certainly true that there are gravity-defying outcomes in the watch industry, such as rapidly escalating prices in the vintage segment during COVID (particularly true when it comes to extremely rare timepieces). However, those trends tend to be the exception rather than the rule.

My book on the history of Rolex marketing is now available on Amazon! It debuted as the #1 New Release in its category. You can find it here.

Last week, Icebox / Swiss Watches GA, a third party retailer of pre-owned watches, officially acknowledged receipt of a lawsuit filed by Rolex USA in the US District Court for the Northern District of Georgia - Atlanta Division. A screenshot of the Icebox / Swiss Watches GA retail location Source: Rolex's legal filing. The cause of action for Rolex's lawsuit against Icebox / Swiss Watches GA is "Trademark Counterfeiting, Trademark Infringement, False Advertising, Designation of Origin, Descriptions, Representations, and Unfair Competition." I've previously covered lawsuits of this sort filed by Rolex against independent retailers who sell modified watches. But this one is an order of magnitude different. Icebox / Swiss Watches GA has some very high-profile clientele. For example, a YouTube video from five years ago entitled "Post Malone Buys Rolex For 21 Savage & Autographs A Bugatti!" has over seven million views (the video content is pretty ...

This may not come as a surprise, but I do not read German-language newspapers on a regular basis. Dial of a vintage Omega Constellation, pie pan. I am, however, keenly interested in a scandal involving the Swatch Group and a "Frankenwatch" Speedmaster which was sold at auction a while back for over $3 million. I won't go into all the minute details here, but the punchline is that Swatch Group bought the watch only to discover that some of its own employees may have been part of a conspiracy to assemble a watch which would be quite rare and important if it were authentic. But, apparently, it was not authentic. When the deception was uncovered, various people who were part of the "inside job" lost employment and, reportedly, legal authorities were notified in Switzerland. I originally wrote about this in 2023, you can read my coverage here . There's been excellent reporting on this matter from many sources (see, for example, this story from Bloomberg). ...

Today, I received a dispatch direct from Le Brassus, aka global headquarters for Audemars Piguet. The email cautions collectors that fraudsters are targeting clients of AP and other brands with potentially bad consequences. In the interest of collector protection, and as a bit of "public service," I'm copying the main body of the AP email below. Be careful out there, always check email headers and double-check with your known contacts at any brands before wiring money, for example: "Cybercriminals are trying to scam customers in every industry and watchmaking makes no exception. At Audemars Piguet we want to be sure that our trusted community is well protected against cyber- criminal exploits. Recently, threat actors have been using spoofing techniques to send fraudulent emails pretending to come from trusted brands, such as ours, in an attempt to deceive individuals into disclosing sensitive information, making payment to illegitimate accounts or engaging in fra...

Thank you for sharing these creative ideas for incorporating wall planter into my home decor. I can't wait to try some of them out!

ReplyDeleteThanks to the author, I found your blog very helpful or informative, I will definitely share it with others also get expert financial solutions, secure loans services, and reliable financial reports with Niyogin Fintech Company. Empowering businesses with fintech services.

ReplyDelete